SVB’s Failure and the Lack of Reserve Requirements

Maybe it's time we raised reserve requirements above zero.

The failures that led to the recent run on Silicon Valley Bank (SVB) are many. SVB chose to invest heavily in long-term interest-bearing assets, which necessarily carry greater interest rate risk, while more than 90% of SVB deposits were not insured by the FDIC. Ultimately, blame should fall squarely on decision makers at SVB. However, we must discuss the institutional framework that let SVB get to this point.

Many have pointed out some of the regulatory features that enabled this crisis. These include the FDIC only insuring deposit accounts up to $250,000 and exempting banks SVB’s size from regulations put in place after the financial crisis of 2008. I would like to point out a recent change that may also have contributed to this bank run: abandoning the reserve requirement.

Until recently, banks in the U.S. were required to hold a percentage of the most liquid deposits as reserves, depending on each bank’s transaction account liabilities. The idea behind a reserve requirement is simply to make it more likely banks would have the funds available in case customers needed to draw upon their deposits. However, banks skirted these requirements starting in the 1990s by using “sweep programs” to transfer funds overnight from accounts subject to the reserve requirement to other accounts that were not. These practices allowed banks to lend more than they otherwise could, which fueled the subprime markets. It got to the point that banks collectively had less than 1% of deposits in reserve.

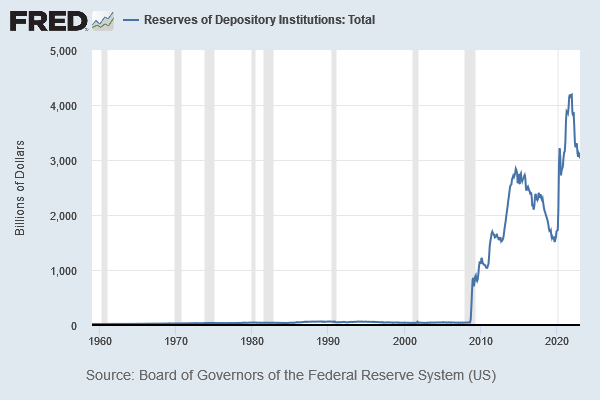

The era of scarce reserves in the U.S. came to an end during the financial crisis of 2008, when the Fed did just about anything it could to encourage banks to lend. Using open market operation to supply enough reserves to push the federal funds rate to zero was not enough. The fed turned to unorthodox measures, namely quantitative easing, through which the central bank spent trillions of dollars on financial assets, leaving private banks flush with cash reserves. The Fed’s approach to monetary policy since then has come to be known as the ample reserves regime. The graph below illustrates the rise in reserves since 2008.

In March of 2020, the Federal Reserve announced it would drop the required reserve ratio on all bank deposits to zero. Part of the reason behind this was a focus on the liquidity coverage ratio, which can be satisfied with reserves and other “high-quality liquid assets.” Also, conventional wisdom held that banks did not need to be “forced” to hold reserves anymore, as the interest payments for reserves, which the Fed started paying in October 2008, would incentivize banks to hold them. Even now, nearly 15 years after implementing the ample reserves regime, aggregate bank reserves are still about $3.03 trillion. Meanwhile, aggregate deposits are around $17.66 trillion. Note that these values imply a reserve ratio just over 17%.

According to SVB’s most recent annual report, at the end of 2022 they held $13.8 billion in cash and cash equivalents, which I will use as an upper bound for their reserves. Meanwhile, SVB also had $173.1 billion worth of deposit liabilities. This means SVB had a reserve ratio no greater than 8%, much lower than the 17% reserve ratio across all banks. This episode illustrates that what’s true at the macro level isn’t necessarily true at the micro level. That is, just because reserves are ample on aggregate doesn’t translate to each bank holding enough to preclude a panic among its depositors.

To me, this episode suggests that paying interest on reserves is not sufficient to entice banks to hold enough to satisfy potentially flighty depositors. We ought to consider raising required reserve ratios above zero again. To ensure that the requirement is effective we should also prohibit the use of the sweep programs banks have used to skirt reserve requirements.

It would not take much to make a difference. For example, suppose regulations were in place such that SVB held 10% of their deposits as reserves, rather than the 8% they actually held. Then SVB would have had an additional $3.5 billion in reserve. Recall that the catalyst for this run was SVB trying to raise $2.25 billion in stock sales to strengthen their balance sheet, an action that rattled SVB’s depositors. With a 10% reserve ratio, SVB would have had $1.2 billion more than they were looking for with the stock sale. It seems reasonable to conclude that in such a scenario the bank wouldn’t have felt the need to sell additional stock to raise cash, this bank run would not have happened, and perhaps this whole crisis would have been averted.

This is certainly one option, with the virtue of simplicity. I've been digging into the Basel III regs and 2023 stress test scenarios, and I think there are a couple specific weaknesses in the current framework:

1. The LCR is calculated on a net basis, and only applies a 25% haircut to incoming HQLAs. So, assuming neutral cash flow on a monthly basis, LCR only assumes you need to hold 25% of the actual predicted 30-day outflows... at best a week's worth of actual HQLA, and given that there's probably some "lumpiness" in when the inflows arrive, potentially less for some weeks of the month.

2. Fed stress tests are completely asymmetric - they test for interest rates and inflation dropping in a recession, and assume the Fed is loosening MP in response. As far as I can see, there's no testing of the reverse scenario, and that's backed up by the Basel III risk weights actively encouraging holding a ton of US Gov securities & relatively HQ MBS's... which both dropped in value as rates rose.